Page 4 of 18

FM10.{8,21} | Consumer Protection Act, Products Liability & Indemnity — SDL Guide

Learning Objectives

- Describe the scope of the Consumer Protection Act 2019 as applied to medical services

- Identify the hierarchy of consumer commissions and their jurisdictional limits

- Define products liability and its relevance to medical devices and pharmaceutical products

- Explain medical indemnity insurance — types, coverage, and why it is essential

- Distinguish civil litigation from consumer forum proceedings in medical negligence cases

INSTRUCTIONS

The Consumer Protection Act 2019 transformed the legal landscape for medical practice in India by giving patients — as consumers — a fast-track, cost-effective forum for compensation claims. Every practising clinician must understand this Act, the parallel products liability framework, and the professional indemnity insurance that protects against these claims.

References

- KSN Reddy — Essentials of Forensic Medicine & Toxicology (textbook)

- BV Subrahmanyam — Modi's Medical Jurisprudence and Toxicology (textbook)

Version 2.0 | NMC CBUC 2024

CLINICAL SCENARIO

A 35-year-old woman undergoes a total knee replacement at a corporate hospital. The implant is manufactured by a reputed orthopaedic device company. Within 18 months, the prosthesis loosens and a revision surgery is required. The manufacturer's own internal data later reveals elevated early revision rates due to a design defect. The patient files complaints against three parties: (a) the orthopaedic surgeon who implanted it, (b) the hospital that procured and used the device, and (c) the manufacturer of the prosthesis.

Which forum has jurisdiction? Who bears liability — the surgeon, the hospital, the manufacturer, or all three? What is the scope of the Consumer Protection Act 2019 in this scenario, and how does products liability differ from professional negligence?

WHY THIS MATTERS

The Consumer Protection Act 2019 (CPA 2019) replaced the 1986 Act and fundamentally expanded consumer rights in India. Medical services were brought within its scope by the Supreme Court in Indian Medical Association v VP Shantha (1995) — a ruling that applied to the 1986 Act and continues to apply under the 2019 Act. CPA 2019 introduced e-filing, a Central Consumer Protection Authority (CCPA), product liability provisions (Chapter VI), and enhanced penalties. Understanding this legislation is not optional — consumer commissions are the primary forum where most medical complaints are adjudicated in India.

RECALL

Recall from the Medical Negligence SDL:

- Civil negligence — adjudicated in civil courts and consumer forums; remedy is compensation.

- Standard of care — the Bolam test; required for civil and criminal negligence analysis.

- Vicarious liability — hospitals may be liable for their employed staff's negligence.

- Medical indemnity — briefly mentioned as a prevention strategy; this SDL covers it in detail.

Also recall from your broader legal training:

• Consumer forum jurisdiction is determined by the value of compensation claimed.

• The burden of proof in consumer proceedings is the balance of probabilities.

Consumer Protection Act 2019: Legal and Professional Context

The Consumer Protection Act 2019 (CPA 2019) is the primary legislation governing consumer rights in India. It replaced the Consumer Protection Act 1986, which was repealed in its entirety. Medical services fall within the CPA 2019's definition of 'service' (Section 2(42)), and medical practitioners and hospitals that charge a fee are treated as 'service providers.' Patients who pay for medical care are 'consumers' under the Act. The 2019 Act applies to services rendered for consideration — services provided free of charge by government hospitals and charitable institutions may not fall within CPA jurisdiction, though this remains an area of evolving judicial interpretation.

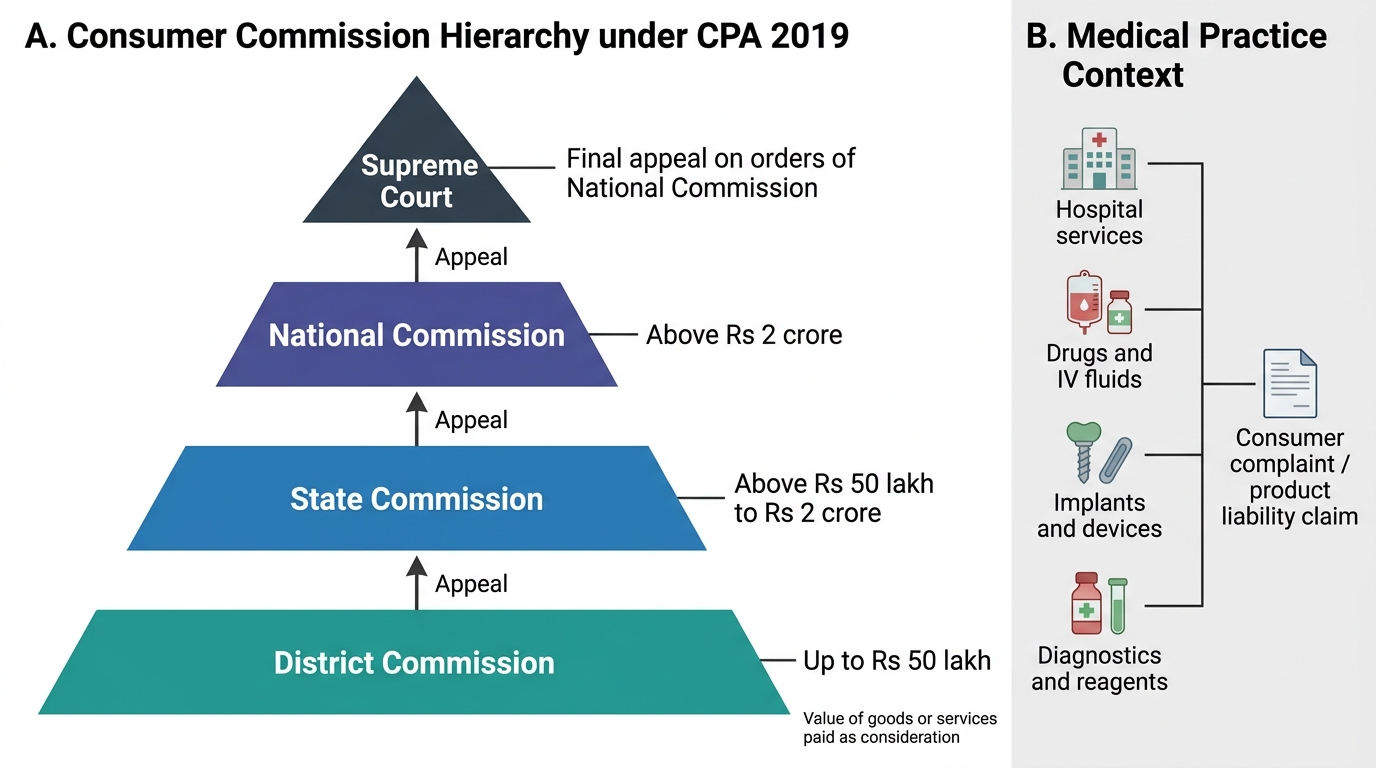

The hierarchy of consumer commissions under CPA 2019 is:

1. District Consumer Disputes Redressal Commission (District Commission) — jurisdiction for claims up to Rs 1 crore.

2. State Consumer Disputes Redressal Commission (State Commission) — original jurisdiction for claims between Rs 1 crore and Rs 10 crore; appellate jurisdiction from District Commission.

3. National Consumer Disputes Redressal Commission (National Commission) — original jurisdiction for claims above Rs 10 crore; appellate jurisdiction from State Commissions.

4. Supreme Court of India — final appellate forum.

Key procedural features of CPA 2019 relevant to medical cases:

- Limitation period: 2 years from the date the cause of action arises (the harm is discovered or reasonably should have been discovered). Courts may condone delay for sufficient cause.

- Complaint can be filed electronically — a CPA 2019 innovation that lowered barriers to access.

- Central Consumer Protection Authority (CCPA): a new regulatory body empowered to investigate widespread consumer harm, recall defective products, and take class action. In medical product cases, CCPA may initiate proceedings.

- Summary procedure: consumer forum proceedings are designed to be quicker and less expensive than civil court litigation; legal representation is not mandatory.

The CPA 2019 does NOT replace the right to pursue civil litigation or criminal proceedings — a patient may simultaneously file in consumer forum, civil court, and police complaint (subject to appropriate legal advice).

Consumer Commission Hierarchy under CPA 2019

Products Liability Under CPA 2019 (Chapter VI)

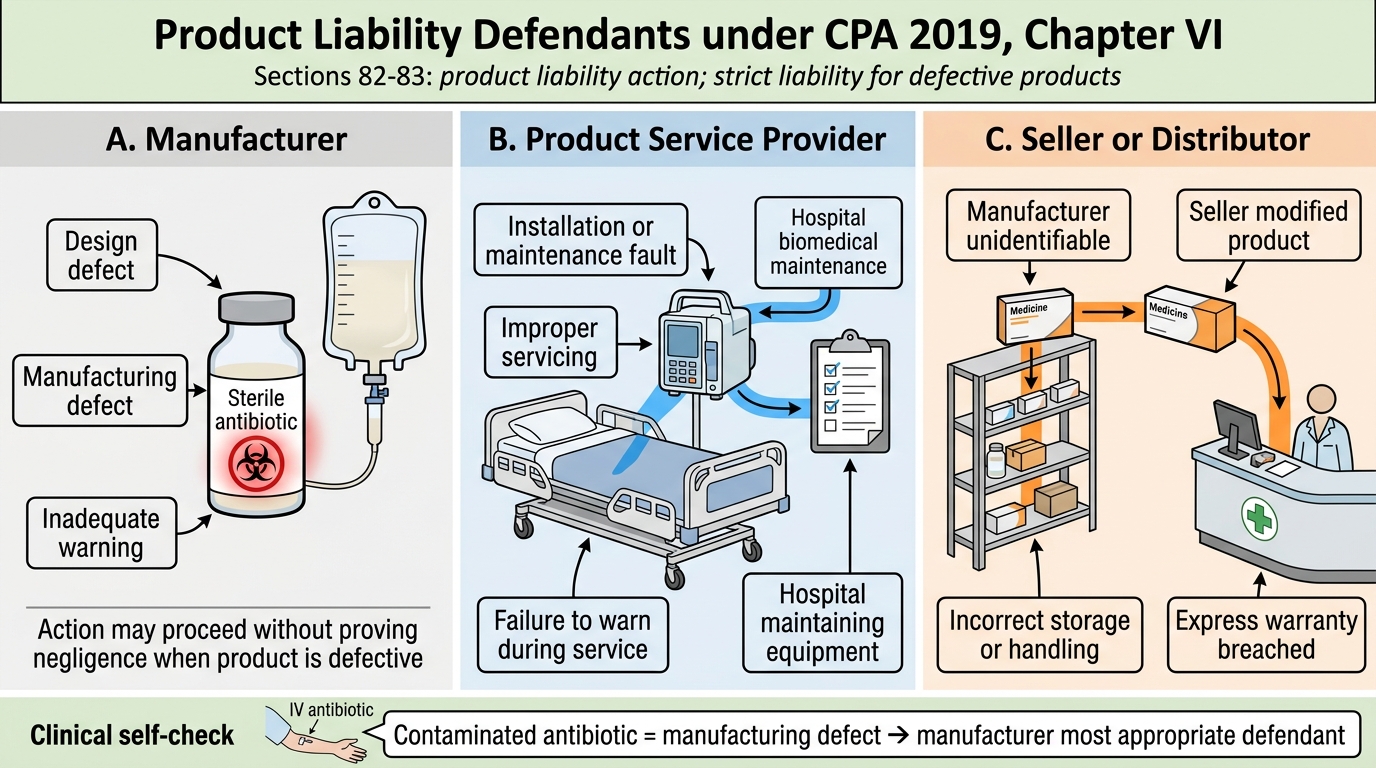

Products liability is the legal responsibility of manufacturers, sellers, and service providers for harm caused by defective products. Chapter VI of the CPA 2019 (Sections 82–87) introduced a statutory products liability framework in India for the first time, departing from the earlier common-law approach. This is of direct relevance to medical practice because the products encountered in clinical settings — pharmaceutical drugs, intravenous fluids, surgical instruments, implantable devices, and diagnostic reagents — are all 'products' within the Act's definition.

Under CPA 2019 Sections 83–84, a product liability action can be brought against:

- The manufacturer — for manufacturing defects (the product deviated from its design), design defects (the entire product line is inherently unsafe), or failure to provide adequate warnings/instructions.

- The product service provider — a person who services or maintains a product (e.g., a hospital maintaining anaesthesia equipment).

- The seller/distributor — if the seller modified the product, the product could not be identified as coming from the manufacturer, the seller failed to exercise due care, or the manufacturer is not within Indian jurisdiction.

Defect categories (Section 2(10)): A product has a 'defect' if it does not conform to the standard required by a mandatory law or regulation, or if it does not match the manufacturer's own express warranty. In the pharmaceutical context, substandard drugs (wrong potency, contamination) are the most common defect category.

Liability without fault (strict liability): CPA 2019 Section 82 creates a product liability action that does not require proof of negligence by the manufacturer — if the product is defective and caused harm, liability may attach. This is a significant departure from traditional negligence-based claims and is especially important for implant and drug litigation.

A doctor who administers a defective drug or implants a defective device may be caught in multi-party litigation alongside the manufacturer. The doctor's own liability turns on whether they acted per standard of care in the selection and use of the product — if the defect was latent and not discoverable on reasonable inspection, the doctor's liability is typically excluded (the defect is the proximate cause). However, using a product known to have quality concerns without adequate warning to the patient may constitute an independent breach of the doctor's duty.

Product Liability Defendants under CPA 2019

SELF-CHECK

A patient receives an intravenous antibiotic that is later found to have been contaminated during manufacturing. She develops a severe local reaction. She files a complaint under the Consumer Protection Act 2019. Against whom can she MOST appropriately bring a products liability action without needing to prove negligence?

A. Only the prescribing doctor

B. Only the hospital that administered the drug

C. The manufacturer of the antibiotic

D. The State Medical Council

Reveal Answer

Answer: C. The manufacturer of the antibiotic

Under Chapter VI (Section 82–83) of the CPA 2019, a product liability action can be brought against the manufacturer of a defective product without proving negligence — this is the strict liability element introduced by the 2019 Act. A contaminated antibiotic is a manufacturing defect. The prescribing doctor's liability depends on whether they acted per standard of care in selection and use; the contamination being a latent manufacturing defect typically removes the doctor from primary liability. The State Medical Council adjudicates professional conduct, not compensation.

Medical Indemnity Insurance: Method and Documentation

Medical indemnity insurance (also called professional indemnity insurance or medical malpractice insurance) is a specialised form of professional liability insurance that protects medical practitioners and healthcare organisations against financial loss arising from claims of negligent acts, errors, or omissions in the course of professional medical practice. In India, the NMC 2020 does not yet mandate indemnity insurance as a licensing condition (unlike the UK, Australia, and the US), but professional and insurance bodies strongly recommend it, and many corporate hospitals require it as a condition of admitting privileges.

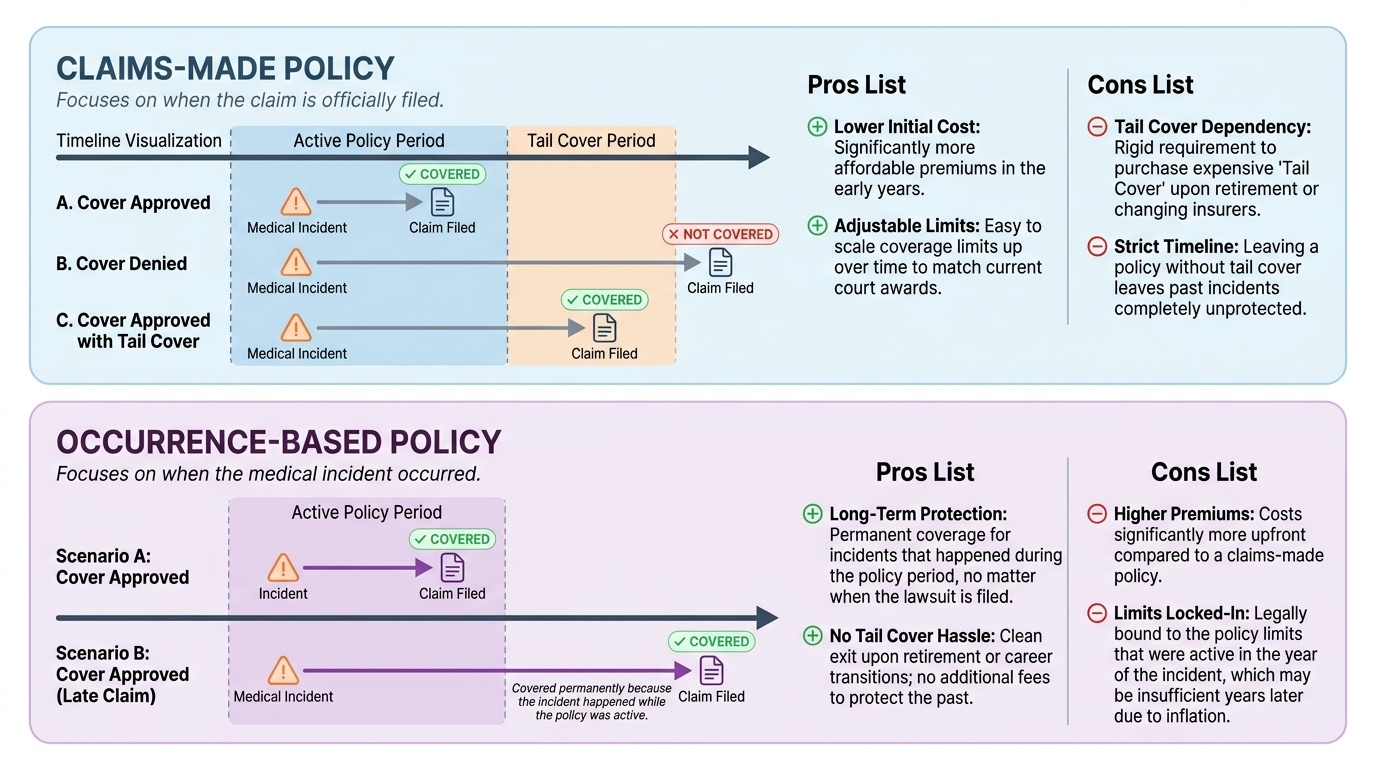

The two principal types of medical indemnity cover are:

1. Claims-made policy: covers claims made (i.e., the claim is filed) during the policy period, regardless of when the incident occurred. This is the most common type for individual practitioners. A critical feature is the 'tail cover' — protection needed after the policy lapses for incidents that occurred during the policy period but for which the claim arrives later.

2. Occurrence-based policy: covers incidents that occur during the policy period, regardless of when the claim is filed. Provides long-term peace of mind but is generally more expensive.

Scope of typical indemnity coverage:

- Legal defence costs — solicitor and barrister fees, expert witness costs.

- Compensation awards — damages awarded by consumer forums, civil courts, or out-of-court settlements.

- Consumer Commission proceedings under CPA 2019.

- Disciplinary proceedings before the NMC or State Medical Councils (professional protection cover).

- In some policies, criminal defence legal costs (up to specified limits).

Exclusions (what indemnity insurance typically does NOT cover):

- Fraudulent, intentional, or criminal acts.

- Services outside the practitioner's registered scope of practice.

- Incidents while practising without a valid registration.

- Claims arising from ownership of premises (covered by property/public liability insurance).

Documentation requirements for a successful indemnity claim: When a claim arises, the insurer requires: (a) the patient's original medical records, (b) the consent form, (c) operation notes, (d) contemporaneous correspondence, and (e) any incident reports filed internally. This underscores why contemporaneous, accurate documentation is the foundation of risk management.

Provided image

Applied Practice: Filing, Defending, and Settling a Consumer Forum Case

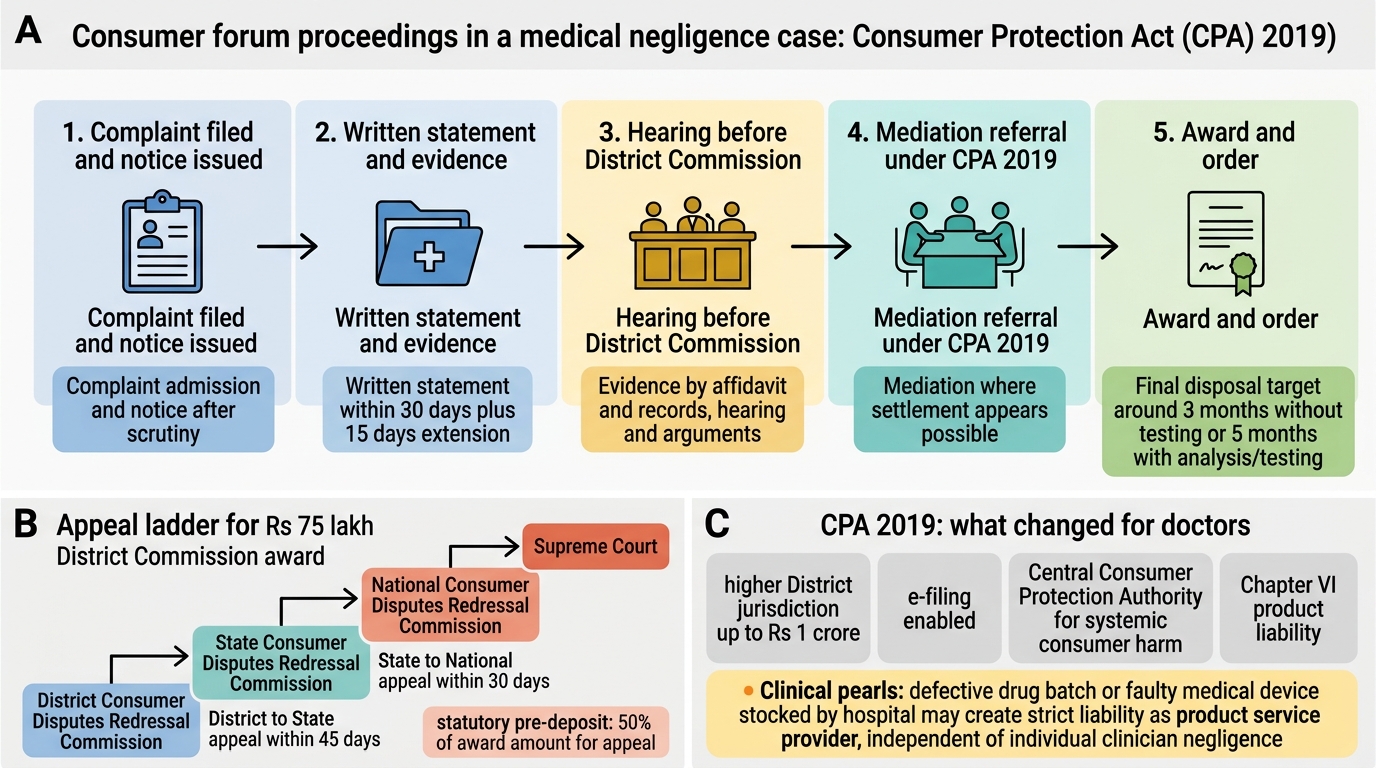

Understanding the practical mechanics of consumer forum proceedings is as important as knowing the law. When a patient files a complaint at a District Commission, the following sequence of events typically unfolds, and the practitioner must respond appropriately at each stage.

Stage 1 — Receipt of complaint: Upon filing, the Commission sends a notice to the opposite party (the doctor/hospital). The opposite party must file a written statement (reply) within 30 days (extendable). At this stage, the practitioner should immediately notify their indemnity insurer, preserve all medical records in their original form, and retain a medico-legal lawyer.

Stage 2 — Submission of evidence: Both parties submit written evidence. The patient's medical records are typically the most critical evidence. Expert opinion is commonly sought. The practitioner's documented clinical reasoning, consent forms, and procedure notes are the primary defence materials.

Stage 3 — Hearing and arguments: Consumer commission proceedings are designed to be less formal than civil court. Oral cross-examination is permitted. Medical expert witnesses explain technical matters to the commission members.

Stage 4 — Mediation (CPA 2019 innovation): The 2019 Act introduced mandatory mediation referral before full hearing where the complaint appears suitable for early resolution. Many medical cases are resolved through mediation with an ex-gratia payment or an apology — without admission of liability. This approach is often in the practitioner's interest: it is faster, cheaper, avoids reputational damage from a public hearing, and an apology has been shown to reduce litigation rates.

Stage 5 — Award and appeal: If the Commission finds in the patient's favour, it may order compensation, direct the return of fees, or impose a penalty. The party aggrieved by the District Commission's order may appeal to the State Commission within 30 days of the order, and from there to the National Commission and Supreme Court.

Key practical principle: Early disclosure + genuine apology + swift mediation is the most cost-effective, reputation-preserving response to a consumer complaint in the absence of serious negligence. Adversarial defence of a clearly indefensible case is strategically, financially, and ethically counterproductive.

Consumer Forum Proceedings in Medical Negligence

CLINICAL PEARL

CPA 2019 vs 1986 Act — what changed for doctors: The 2019 Act raised jurisdictional thresholds (District Commission now covers up to Rs 1 crore, previously Rs 20 lakh), introduced the Central Consumer Protection Authority (which can investigate systemic consumer harm), added the statutory product liability Chapter VI (strict liability for manufacturers), and enabled e-filing of complaints. The most clinically significant addition is the product liability chapter — a hospital that stocks a defective batch of a drug or a faulty medical device may face strict liability as a 'product service provider' under CPA 2019, independent of whether the individual clinician was negligent.

SELF-CHECK

A patient is awarded Rs 75 lakh compensation by the District Consumer Disputes Redressal Commission against a private hospital. The hospital wishes to challenge this order. Which is the CORRECT forum for the first appeal?

A. National Consumer Disputes Redressal Commission

B. High Court

C. State Consumer Disputes Redressal Commission

D. Supreme Court of India

Reveal Answer

Answer: C. State Consumer Disputes Redressal Commission

Under the Consumer Protection Act 2019, appeals from a District Commission lie to the State Consumer Disputes Redressal Commission within 30 days of the District Commission's order. The National Commission is the forum for original jurisdiction above Rs 10 crore and for appeals from the State Commission. The High Court and Supreme Court may be approached for constitutional or appellate matters but are not the first port of call for a consumer forum appeal.

KEY TAKEAWAYS

The Consumer Protection Act 2019 applies to paid medical services; medical practitioners are 'service providers' and patients are 'consumers.' The three-tier commission structure (District up to Rs 1 crore → State Rs 1–10 crore → National above Rs 10 crore) provides a fast-track compensation forum. The 2-year limitation period runs from when the cause of action arises. Chapter VI of CPA 2019 introduced statutory products liability — manufacturers face strict liability (no need to prove negligence) for defective products including drugs and implants. Doctors caught in multi-party product liability cases are insulated if they acted per standard of care and the defect was latent. Medical indemnity insurance — claims-made or occurrence-based — covers legal defence and compensation costs; requires current registration and good documentation. CPA 2019 (not 1986) is the applicable statute; know the enhanced jurisdictional thresholds and the new CCPA.

REFLECT

You are about to start independent clinical practice. You discover that your hospital does not require medical indemnity insurance and that a colleague has never had a policy. Reflect on the arguments for and against making indemnity insurance mandatory for all registered practitioners in India. What systemic changes to the consumer forum system would best balance patient access to compensation with protection of practitioners from vexatious claims? How would you personally ensure you are adequately protected?